For most of my adult life, my budget had a recurring villain. The Surprise Bill. Car registration. The vet. Six months of insurance, due all at once. Every time, the same scene played out. A good month ruined, an awkward transfer out of savings, and me muttering “where did that come from?”

Here’s the embarrassing truth I eventually had to face. None of these were surprises. Every single one was scheduled, predictable, and in one case printed on a letter that had been stuck to my fridge for a month. They only felt like ambushes because I budgeted month to month while my bills lived on a yearly calendar.

Sinking funds fixed this so completely that paying bills is now weirdly satisfying. Here’s the system, and the six funds that run it.

What a sinking fund actually is

Take a bill that arrives occasionally. Divide it by the number of months between arrivals. Save that slice every month into a labeled pot. When the bill lands, the pot pays it.

That’s the entire trick. A $360 insurance premium due every six months stops being a $360 punch and becomes a painless $60 line item.

The magic is psychological as much as mathematical. The money is already gone from your spending brain. You never miss it, and the bill loses all of its drama.

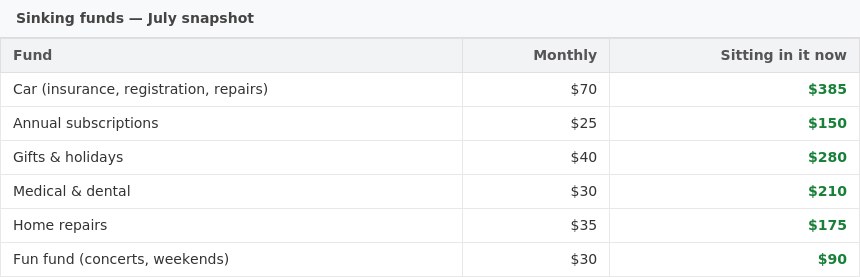

The six funds I actually run

1. Car stuff: $70 a month

Registration, insurance, and an allowance for repairs. Cars don’t break monthly but they absolutely break yearly. When the brake job came in at $410 last fall, the fund had $530 waiting. I paid it with the emotional energy of buying groceries.

2. Annual subscriptions: $25 a month

Every yearly renewal added up and divided by twelve. Streaming, software, memberships. Building this fund forced me to list all my annual charges in one place, and that list immediately got two of them cancelled. The list was scarier than the total.

3. Gifts and holidays: $40 a month

December used to be a financial crime scene. Birthdays, holidays, wedding season. It’s all one fund now. Saving for gifts in March feels ridiculous right up until November, when it feels like genius.

4. Medical and dental: $30 a month

Copays, glasses, and the crown my dentist keeps foreshadowing like it’s a plot point. Health costs are the classic surprise that is actually a certainty with a flexible date.

5. Home repairs: $35 a month

Something in every home is quietly planning to leak. This fund means the water heater’s eventual betrayal is already paid for.

6. The honest fun fund: $30 a month

Concert tickets. A weekend away. Not an emergency by any definition, but unfunded fun always ended up raiding the other categories anyway. Giving it its own pot protects everything else. It’s the same lesson as zeroing out fun money. Pretending a need doesn’t exist never deletes it.

Where to keep them

Mine live in one savings account with a simple note tracking each fund’s share. Some banks offer sub accounts or buckets, which is tidier. It honestly doesn’t matter. The label is the technology. The account is just where the labels sleep.

Starting when money is tight

$230 a month across six funds sounds impossible when things are stretched. So don’t start there. Start with one fund, whichever bill hurt most last time, and $20 a month.

The point in month one isn’t coverage. It’s the shift from “bills happen to me” to “bills are scheduled, and so am I”. Coverage builds itself from there, one boring month at a time.

Two years in, my budget hasn’t been wrecked by a surprise since. The bills didn’t change. I just stopped being surprised by appointments.

Photo by 401(K) 2013, source (CC BY-SA).

Amelia writes Cents That Count from her kitchen table. She has quit four budgeting apps, run one no spend month, tracked every small purchase for 60 days, and still buys coffee. Everything here is tested on a real, ordinary budget first.

More about this blog →